Executive Summary

- The express car wash market is saturated after a decade of private equity consolidation; commercial truck wash presents the same pre-consolidation profile today: fragmented supply, recurring demand, and no institutional platform.

- Automated truck wash equipment crossed its quality threshold in roughly the last two to three years. 3D vehicle profiling, touchless and hybrid formats, and fleet account software removed the barriers that kept the category manual.

- When institutional capital enters a wash category, early operators holding built, permitted, cash-flowing sites become the acquisition targets. That is what the car wash record shows, and truck wash now fits the pattern.

- The binding constraint is not equipment or demand. It is development: finding, entitling, and building sites that can handle truck geometry. That is where first-time owners stall and where the window is won or lost.

There is no institutionally backed, multi-site, automated truck wash development platform in the United States. Not one. This paper explains why that gap exists, why it was rational until roughly the last twenty-four months, what changed in wash technology to open it, and why the operators who move first, before institutional capital repeats the playbook it just ran in express car wash, stand to capture the position. It also deals honestly with the counterarguments, because a thesis that cannot survive its skeptics is not worth building on.

The Missing Platform

Start with the fact that should not be possible.

The American express car wash industry absorbed billions of dollars of private equity capital over the past decade. Firms including Leonard Green, Golden Gate, KKR, Warburg Pincus, and Oaktree built and traded platforms of hundreds of locations, and express tunnels grew from a niche format into roughly half the North American car wash market. Consolidation in that category is now so far along that its own trade association reports market saturation as the industry's top operational concern, and cities from Michigan to Texas are passing moratoriums on new tunnels. For express car wash operators and investors asking what comes after saturation, commercial truck wash is the closest undeveloped adjacent category.

One asset class over, on the same interstates, sits commercial truck wash. Demand is settled: nearly 15 million registered commercial trucks, more than 580,000 active motor carriers, and washing that is increasingly required rather than optional, driven by corrosion economics, inspection outcomes, shipper appearance standards, and food-chain hygiene rules. The category leader, Blue Beacon, has spent five decades building a respected network of more than 110 hand-wash locations. Beyond it, supply is thin: regional independents, single sites, and travel-plaza bays, with no national number two.

And yet: there is no institutionally backed, multi-site, automated truck wash development platform in the United States. None. The private equity transactions that touch the space, such as Fleetwash and Kept Companies, are mobile fleet-washing services, crews that drive to a customer's yard. The fixed-facility category, the direct analog to the express tunnel, has attracted essentially no institutional development capital.

A gap like that demands an explanation, because "everyone missed it" is almost never the real answer. The honest question, and the one a skeptic should ask first, is this: if the opportunity is real, why has nobody built it? This paper answers that question directly, because the answer is also the reason the window is open right now and was not open five years ago.

One more thing worth saying up front. Almost everyone who enters this industry enters through the equipment: they talk to a manufacturer, get a quote, and get excited. The equipment manufacturers are excellent at what they do, and the newest generation of their systems is the subject of a full section below. But equipment manufacturers are not land developers, and a wash system without a found, controlled, entitled, and built site is a quote in a drawer. Anyone asking how to start a truck wash business eventually discovers the same thing: the equipment is the easy part, and development is the constraint. Holding that distinction in mind is the difference between reading this paper as a spectator and reading it as an operator.

Why Nobody Has Built It: The Skeptic's Case, Answered

Three serious objections stand between this thesis and a signature. Each deserves a straight answer.

Objection one: if it were viable, Blue Beacon would have automated already

Blue Beacon's moat deserves more credit than the automation-versus-labor framing usually gives it. Its advantage is not merely crews; it is five decades of interstate site positioning, fleet trust, driver habit, dispatch familiarity, and hard-won operating and environmental experience. Its hand-wash model also does things automation historically could not: crews adapt to chrome packages, custom lights, tankers, flatbeds with strapped loads, and every irregular configuration a Class 8 fleet can present, without damaging any of it.

That is precisely the point. For most of the category's history, manual labor was not the weak legacy format; it was the only format that could deliver acceptable quality across real-world truck geometry. Early automated truck equipment struggled with mirrors, stacks, and trailer variety, missed dirt or caused damage, and gave automation a deserved reputation problem among fleets. A rational operator, and Blue Beacon is a very rational operator, does not replace a working labor model with technology that washes worse. The absence of an automated platform was not an oversight. It was a correct reading of the equipment available at the time.

Objection two: if the corridors were valuable, Pilot and Love's would have done it

Berkshire Hathaway's staged, multi-billion dollar acquisition of Pilot Flying J and BP's $1.3 billion purchase of TravelCenters of America prove that institutional capital values freight corridor service real estate. They do not prove anything about truck wash economics, and this paper will not pretend they do. Travel centers are fuel, convenience retail, food service, and parking businesses; washing is a high-water, environmentally sensitive operation outside their core model, which is exactly why most have left it to third parties. The right reading is narrower and still useful: the land is validated, the operation is unclaimed. The travel center giants' absence from washing is not evidence the business is bad. It is evidence the business is nobody's job yet.

Objection three: freight tonnage is not wash demand

Correct, and worth conceding cleanly. A large share of freight moves in fleets that wash in-house at their own distribution centers or contract mobile services to their yards. Macro tonnage growth does not flow line-by-line into retail wash volume. What it does establish is that the underlying vehicle base is enormous, growing, and durable: the American Trucking Associations projects truck tonnage rising from an estimated 11.27 billion tons in 2024 to 13.99 billion tons by 2035, and the first quarter of 2026 was the strongest quarterly tonnage performance since 2017. The retail wash opportunity lives in the segments that cannot wash in-house: over-the-road carriers between terminals, owner-operators, regional fleets without yard infrastructure, RV and large-vehicle owners, and food-grade haulers needing documented washouts on the road. Sizing that capture is site-specific work, which is a development question, not a spreadsheet question, and this paper returns to it at the end.

Notice what all three answers have in common. None of them says the skeptics were wrong. They say the skeptics were right, until the equipment changed. That is the next section, and it is the heart of the matter.

What Changed: The Equipment Generation That Opens the Category

Roughly the last two to three years, and especially the last twelve months, have produced a generation of large-vehicle wash technology built specifically to solve the problems that kept the category manual. Big Rig Development Group is equipment-agnostic and makes no performance claims of its own; what follows is what the manufacturers and industry equipment guides themselves report, across multiple competing systems.

3D vehicle profiling changed the geometry equation

The defining advance is dimensional scanning. Current systems, including D&S Car Wash Supply's IQ MAX, LazrTek's laser-profiling gantries, and Westmatic's robot-controlled arms, scan each vehicle with light grids, lasers, or computer vision, build a profile of its actual contours, and direct the wash cycle around that profile. D&S markets the IQ MAX's ability to follow intricate details and add-ons such as ladders, stacks, lifts, mirrors, and booms with minimal labor, on vehicles ranging from a sprinter van to a semi trailer, in a cycle it advertises at under fifteen minutes. Whatever brand a project selects, the capability itself is the story: automated equipment can now accommodate a much broader range of truck geometry than the fixed-pattern systems that once made manual crews the more practical choice. The historical objection to truck wash automation was real, and this generation of equipment has substantially reduced it. Edge cases remain, irregular loads, heavy accessory packages, damaged equipment, and most retail sites still run a lane attendant for loading, inspection, and pre-wash, but the geometry limitation that kept the category manual is no longer the barrier it was.

Touchless, friction, and hybrid formats address the damage objection

The second fleet objection was brush damage to paint, wraps, and decals. The current market answers it with configuration choice: touchless high-pressure systems for reefers, wrapped trailers, and high-gloss livery where zero contact matters; friction for heavy mud and bonded road film that pressure alone struggles to break; and hybrid systems from manufacturers including InterClean, Westmatic, and KKE that combine both in one line. Fleets that preferred hand washing for damage reasons now have a no-contact automated option, which addresses one of the largest historical quality concerns. It does not settle every case: some fleets still specify manual washing for inspection, detailing, or heavily soiled equipment, and configuration has to match the vehicle mix a site actually serves. But the blanket quality argument for keeping the entire category manual no longer holds.

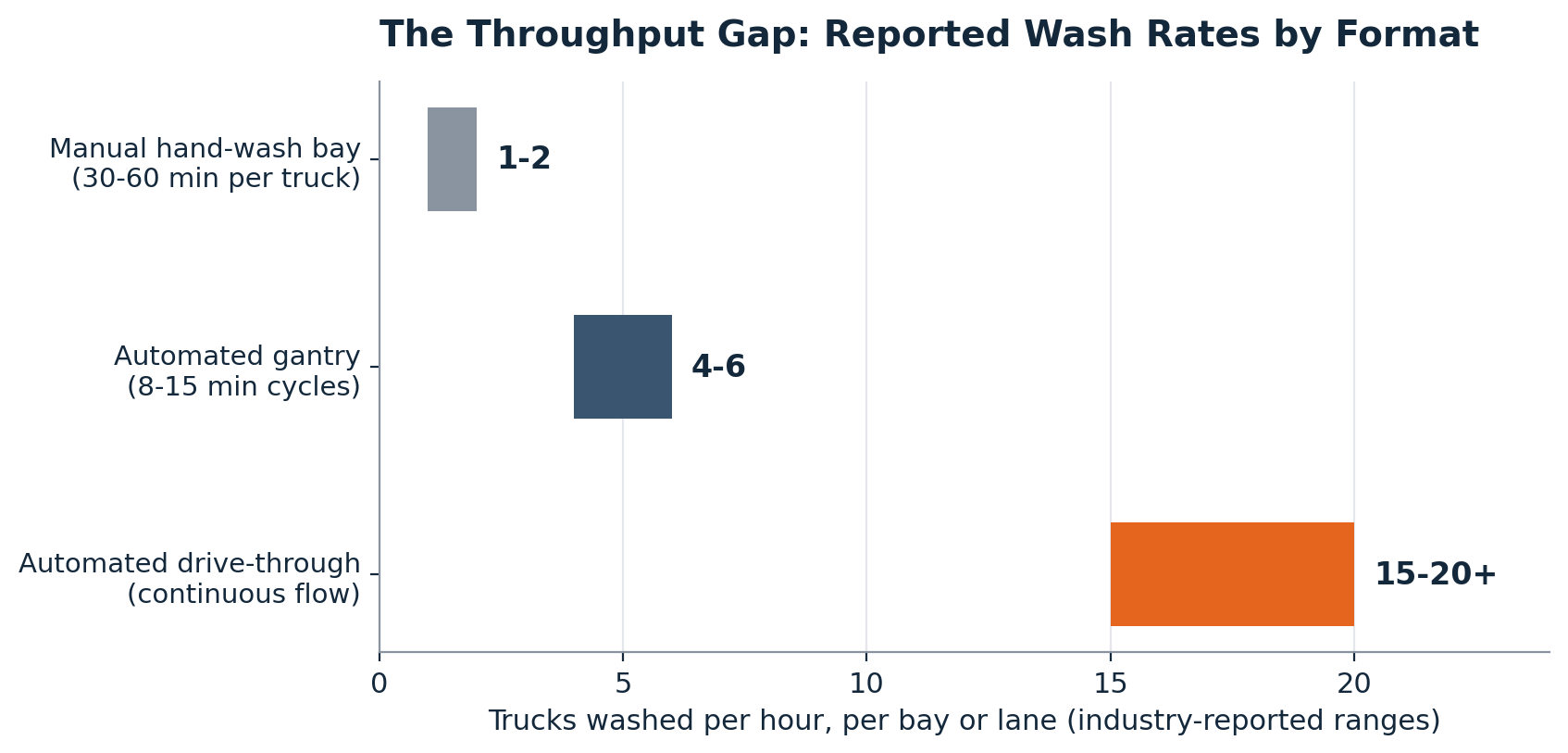

Throughput is the economic wedge

Industry equipment guides put manual hand-wash service at roughly thirty to sixty minutes per tractor-trailer. The same guides report automated gantry systems cycling in eight to fifteen minutes, roughly four to six trucks per hour per bay, and drive-through systems, where the truck moves through stationary arches in a continuous flow, at fifteen to twenty or more trucks per hour, with several manufacturers advertising cycles under five minutes. These are rated cycle times, not operational throughput: real-world site volume runs lower once driver loading, payment, queueing, pre-wash on heavily soiled vehicles, and mixed geometry are counted, and a mixed retail lane will not hit continuous-flow fleet numbers. The directional gap is still large, and it is the point. On economics, D&S publishes a vendor-modeled comparison for fleet washing at roughly $125 per automated wash against $250 or more for manual methods once labor and downtime are counted. That figure is a manufacturer scenario built on specific labor, utilization, and utility assumptions, not an audited industry benchmark, and it excludes the higher equipment capital and specialized maintenance automation carries; a real project has to model its own numbers. What survives the caveats is the structural direction: automation moves more trucks per labor hour, and in this category labor hours and downtime are the cost that matters.

Figure 1 data: Manual hand-wash bay (30 to 60 minutes per truck): 1 to 2 trucks per hour. Automated gantry (8 to 15 minute cycles): 4 to 6 trucks per hour. Automated drive-through (continuous flow): 15 to 20+ trucks per hour.

Why throughput is the whole game in this category: the customer is a driver on federally regulated hours of service or a fleet manager measuring downtime, and a truck only earns when it is moving. Every hour in a wash queue is non-revenue time on a $150,000-plus asset. A facility that washes a truck in minutes instead of most of an hour is not selling a nicer wash; it is selling the driver's day back.

The supporting stack matured with it

- Water reclamation: manufacturers including Westmatic advertise systems recycling up to 85 percent of wash water under favorable operating conditions, using ozone and electroflocculation treatment. Truck wash effluent remains a serious engineering and permitting item, and no honest paper minimizes it. Reclaim is not set-and-forget: it carries ongoing sludge handling, disposal cost, and municipal compliance risk, and actual recovery varies with load and maintenance. What modern systems change is that it moves from a likely project-killer to a designed-for, managed cost, which is exactly the kind of item experienced development management exists to scope before capital is committed.

- Undercarriage and chassis wash: dedicated wheel blasters and chassis systems target the road salt and de-icing chemicals that drive corrosion, the single largest maintenance argument for frequent washing in the salt belt.

- Fleet account software: RFID vehicle tags, cloud-based per-vehicle tracking, consolidated invoicing, app management, and remote monitoring, the same subscription infrastructure that made car wash membership economics famous, now ships off the shelf for large-vehicle operations.

- Remote monitoring: current systems are web-connected for remote programming, wash counts, and service diagnostics. On-site staff still handle chemicals, reclaim, and physical maintenance, but remote oversight is what makes a lean-staff, long-hours retail truck wash operationally realistic.

And the manufacturers are already moving

This is not a forecast; it is observable. D&S exhibited the IQ MAX at NATSO Connect, the travel center industry's trade show, explicitly pitching large-vehicle wash to truck stops and travel centers, and other manufacturers are marketing retail and commercial truck wash packages the same way. The equipment side of the industry has read the opening and is building for it. The movement runs on both sides of the wash industry: several companies building large-vehicle systems today grew out of car wash equipment lines, and for car wash equipment manufacturers watching their own category tighten, large-vehicle wash is the natural adjacent line the market is signaling for. What the equipment companies cannot supply is the other half of the project: the land.

The precedent for what happens next

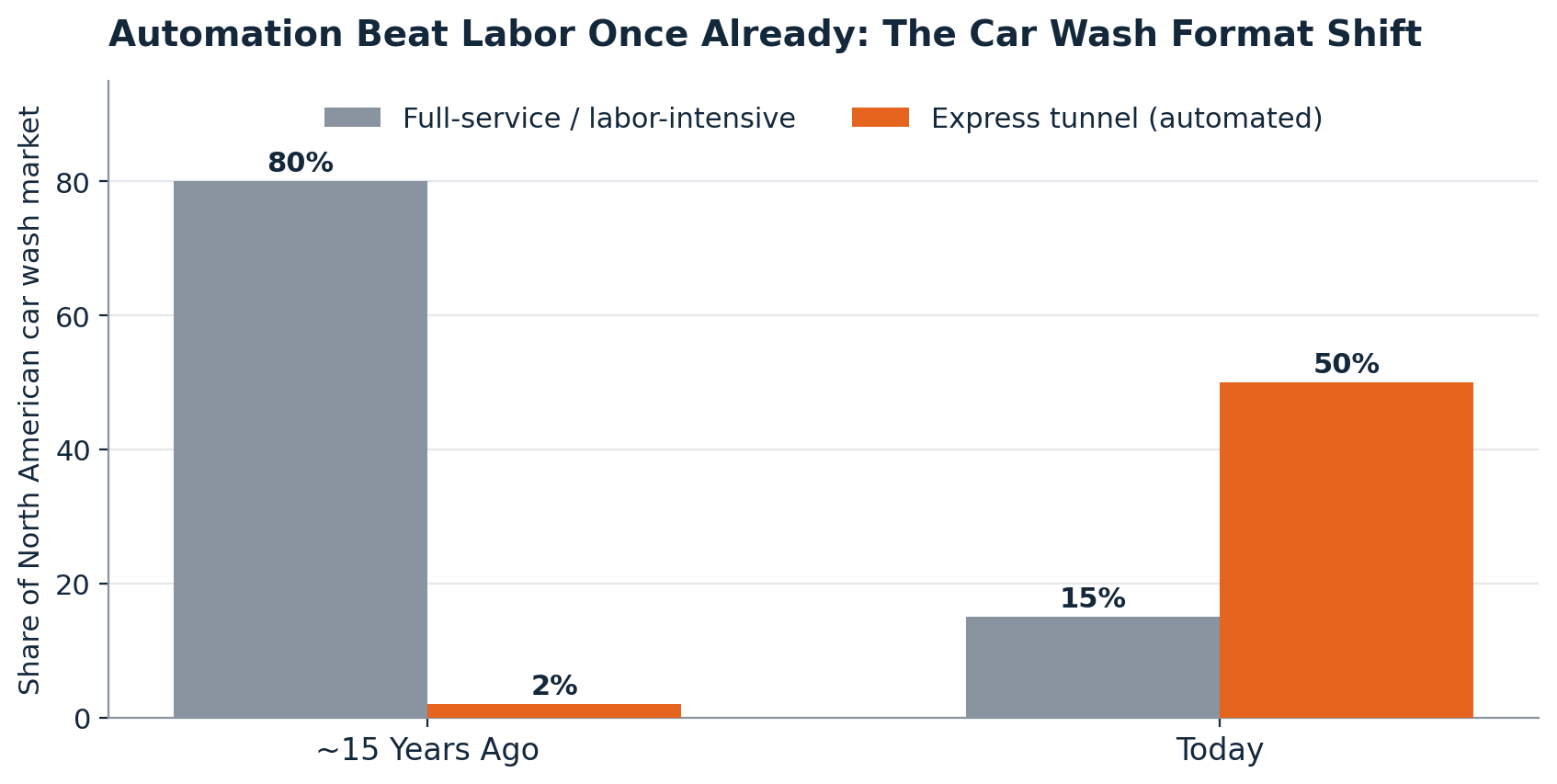

The wash industry has already run this experiment once. When conveyor automation and subscription software matured in passenger car washing, the labor-intensive incumbent format did not adapt in place; it lost the market. Full-service washes fell from roughly 80 percent of the North American market to about 15 percent while automated express tunnels grew from a niche to roughly half, over about fifteen years.

Figure 2 data: Full-service (labor-intensive) car wash fell from roughly 80 percent of the North American market to roughly 15 percent. Automated express tunnels grew from a niche format to roughly 50 percent, over approximately fifteen years.

That chart is usually read as car wash history. Read it as what it actually records: what happens in a wash category when automation crosses the quality threshold against a labor incumbent. Truck wash equipment appears to have crossed that threshold for many fleet and retail applications, later and less completely than passenger car wash did, but far enough that the format math has changed. The incumbent's five decades of excellence at the labor model, the very thing that earned its position, is also what makes retrofitting automation across a hundred-plus site network a slow, expensive proposition, which gives new entrants a window measured in years, not months.

The Capital Precedent: What Car Wash Teaches About Timing

The express car wash consolidation is worth exactly one section here, because it answers one question: what happens to early operators when institutional capital discovers a fragmented wash category with an automation wedge.

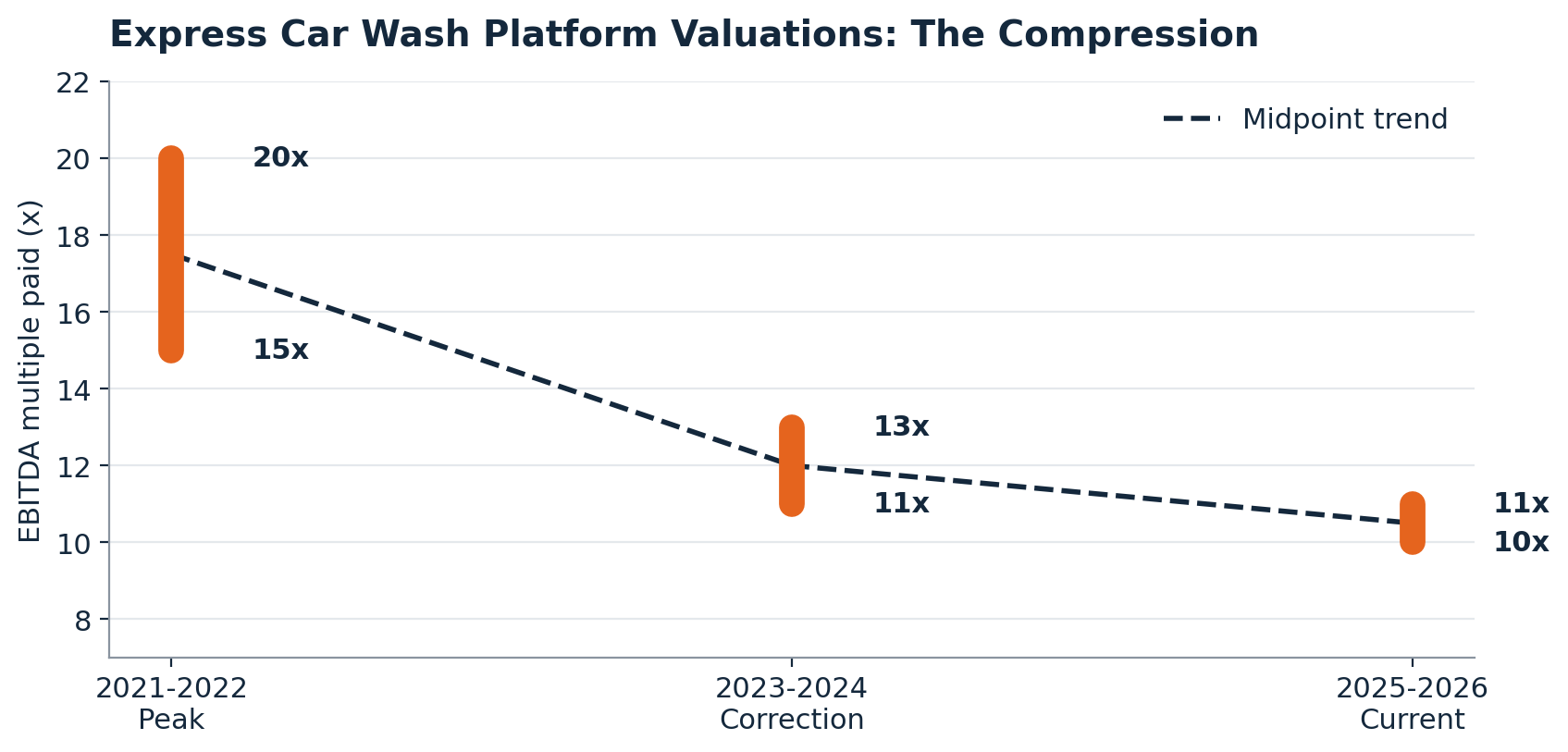

Over roughly a decade, sponsors including Leonard Green, Golden Gate, KKR, Warburg Pincus, and Oaktree built express car wash platforms through acquisition far more than construction. At the 2021 to 2022 peak they paid from the mid-teens up to 20 times EBITDA for premier platforms, and premium prices for well-sited independents, because buying an operating site with permits, membership revenue, and history was faster and surer than entitling raw land. The independent operators who had built three, five, or ten good locations before the wave were not the competition when capital arrived. They were the product.

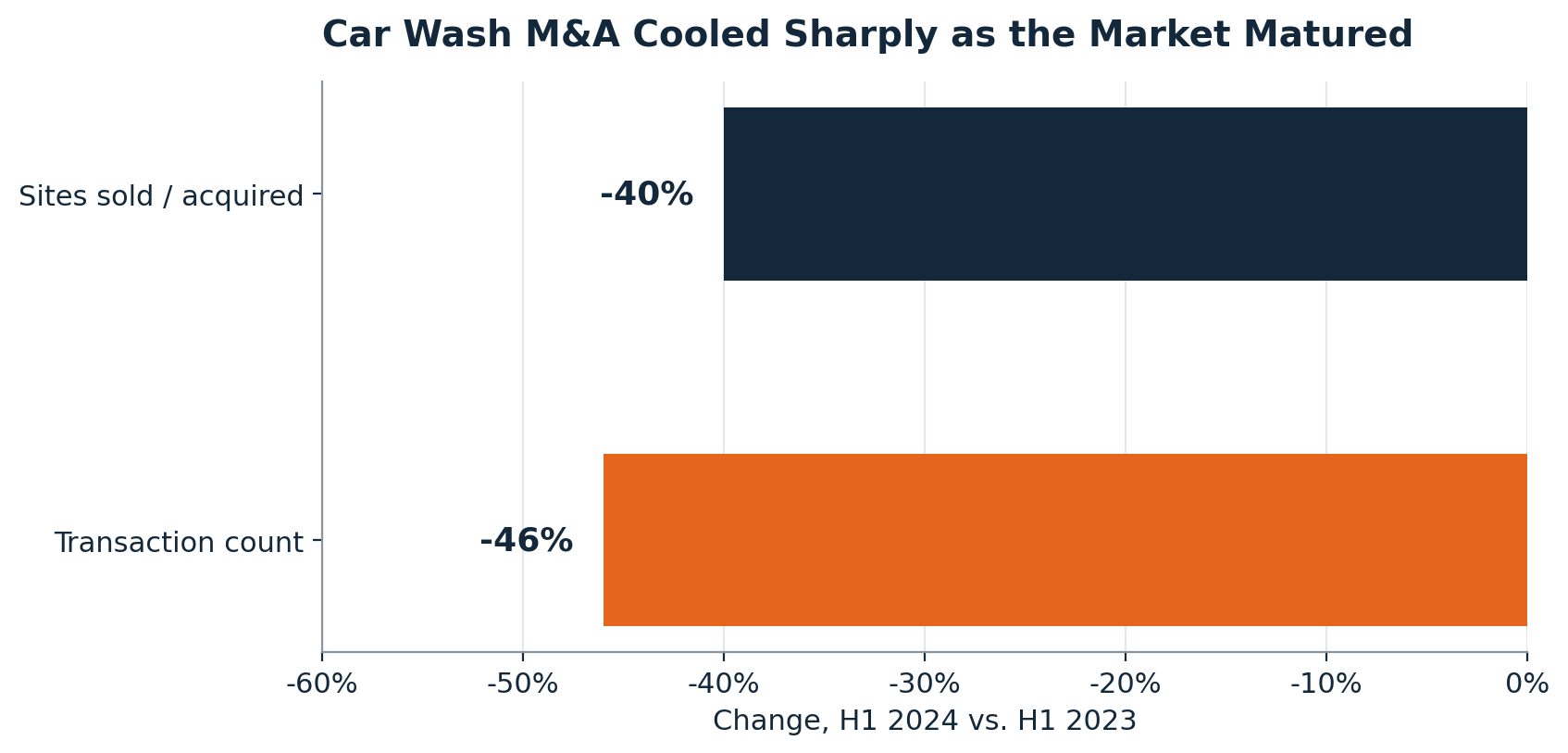

The same record also shows what maturity looks like. Car wash M&A transaction count fell approximately 46 percent in the first half of 2024 versus the prior year, platform pricing compressed to roughly 10 to 11 times EBITDA, ZIPS filed Chapter 11 under $654 million of debt, and the International Carwash Association's own 2026 surveys now rank saturation as the industry's top concern. Capital is still active in car wash, and an exit wave is expected as 2020 to 2022 vintage funds reach the end of their hold periods. But the open-field, greenfield phase is over in the strongest markets.

Figure 3 data: Car wash M&A transaction count fell approximately 46 percent, first half 2024 versus first half 2023.

Figure 4 data: Peak platform pricing ran from the mid-teens up to 20x EBITDA in 2021 to 2022, compressing to roughly 10 to 11x by 2024 to 2026.

To be precise about what this precedent does and does not prove: it does not guarantee that truck wash consolidates on any timeline, and the categories differ in real ways, consumer subscriptions versus fleet contracts among them. What it proves is narrower and sufficient: when a wash category offers fragmentation, recurring demand, real assets, and a maturing automation wedge, institutional capital has shown exactly how it behaves, and the operators already holding built positions captured the premium. Truck wash now presents that same profile to a capital base actively hunting its next category. Whether the wave arrives in three years or seven, the asymmetry for an early operator is the same, and it is the subject of the next section.

The Strategic Play: Own the Position Before It Has a Price

If you have been circling this industry, whether as an express car wash operator watching your category tighten, an investor who ran the tunnel numbers and found the good corners taken, a travel center or truck stop operator with freight traffic already parked on your lot, or someone already holding an equipment quote, here is the play the evidence supports.

It is not out-building Blue Beacon. It is being early and regional:

- One facility proves the model: a well-sited automated wash on a strong freight corridor, with fleet accounts signed, in a trade area where drivers today have one option or none.

- Three to five facilities make a platform: route density for fleet contracts, shared overhead, a brand drivers recognize across a lane, and control of scarce, hard-to-entitle real estate.

- The operating history becomes the asset: sites, permits, fleet contracts, throughput data, and a trained team are what an acquirer pays for, and what cannot be assembled quickly once a category heats up.

The position is asymmetric. If institutional capital enters truck wash the way it entered car wash, an operator holding built, permitted, cash-flowing sites in a market with very few of them is the acquisition target, and scarcity sets the price. If the wave never comes, the operator owns a contract-backed service business in an underserved category, sitting on freight corridor real estate that the largest investors in America have already shown they value. Building now is rewarded in both scenarios. Waiting is rewarded in neither, because the cost of entry only moves one direction once the first institutional platform announces itself: land prices on the best corridors move, equipment lead times stretch, and the first-mover position stops being available at today's cost.

What about the fleet contracts?

The fair worry for a first-time owner: how does a single-site operator sign fleets before the facility exists? The answer is that fleet demand is qualified during site selection, not after opening. The same corridor analysis that justifies the land identifies the carriers, distribution centers, and food-grade haulers within routing distance, and those conversations happen while the site is under contract and in entitlement, not after the ribbon cutting. Drive-up traffic from owner-operators, RVs, and pass-through carriers anchors early volume; fleet agreements layer on as the facility proves turnaround time. This is standard commercial development sequencing, and it is one more reason the development phase, not the equipment phase, decides the outcome.

The honest economics

This paper deliberately publishes no pro forma, and the reason matters. Truck wash unit economics are driven by variables that only exist at the site level: land basis, corridor traffic composition, utility and wastewater conditions, entitlement timeline, equipment configuration, and the fleet base within routing distance. Any generic IRR printed here would be an invention, and inventions are how first-time owners get hurt. The disciplined sequence is the reverse: qualify the site, model the specific project, then commit capital. Which is the last argument of this paper, and the most practical one.

What an Early Mover Actually Does: The First Twelve Months

The opportunity only converts through development, so here is what the work concretely looks like for an operator starting now. No step on this list involves buying equipment; the equipment decision arrives on schedule once the site earns it.

- Pick the lane: select one or two freight corridors using traffic composition, fleet and distribution density, and competitive supply, including where the nearest existing wash options are and what they can and cannot serve.

- Screen candidate sites against truck geometry: usable acreage, 40-to-55-foot turning paths, 180-to-420-foot stacking, full-movement access. Most parcels fail here, which is why this screen comes first.

- Pre-screen entitlement and utilities: zoning posture toward heavy vehicle uses, wastewater capacity and pre-treatment requirements, water availability, and the jurisdiction's review process, before money is at risk.

- Qualify the demand base: identify the carriers, DCs, food-grade haulers, and RV traffic within routing distance and open the fleet conversations early.

- Control the land: negotiate the purchase or lease with contingency periods that protect the project through feasibility and entitlement.

- Entitle: assemble the architecture and engineering team, drive the site plan, and submit a complete, defensible municipal application.

- Select equipment and configuration: with the site's geometry, volume profile, and water conditions known, the touchless, friction, or hybrid decision, and the manufacturer decision, can be made on facts.

- Build: general contractor procurement, construction management, equipment installation coordination, and the path to certificate of occupancy.

Twelve months of that sequence, executed well, puts an operator under construction on a corridor position that did not exist in the market a year earlier and cannot be quickly replicated by whoever arrives second.

Where Projects Live or Die

Truck wash and car wash share underwriting fundamentals: traffic, access, entitlement risk. What differs is what each demands of a site, and the thresholds are higher across nearly every factor.

| Site Factor | Express Car Wash | Commercial Truck Wash |

|---|---|---|

| Site acreage | 0.8 to 1.5 acres typical | 1 to 3+ acres usable |

| Turning radius | Standard passenger vehicle | 40 to 55 ft for a 53-ft trailer |

| Stacking depth | 10 to 20 cars (100 to 200 ft) | 3 to 6 trucks (180 to 420 ft) |

| Access | Right-in / right-out acceptable | Full-movement strongly preferred |

| Traffic pattern | High-VPD arterial, retail | Freight corridor, distribution proximity |

| Wastewater | Standard pre-treatment | Enhanced pre-treatment, reclaim systems |

| Revenue model | Membership subscription | Fleet contract, per-wash volume |

| Entitlement risk | Moderate | Elevated (heavy vehicle operations) |

The right-hand column is the gauntlet. A site that fails on turning radius or stacking depth fails permanently; no operating decision fixes bad geometry. Wastewater is a genuine engineering and permitting workstream, not a checkbox, and heavy vehicle uses draw elevated municipal scrutiny, so the application has to be complete and defensible the first time. Most first-time wash owners do not stall on ambition or capital. They stall here, in the gap between holding an equipment quote and holding a certificate of occupancy.

National brands close that gap with in-house real estate teams. Most people building their first truck wash do not have one, and the equipment manufacturers, however excellent at what they build, are not land developers. The practical requirement is simple to state: treat site selection through certificate of occupancy with the same seriousness as the equipment decision, and put experienced development management on it from day one. The equipment makes the wash work. The real estate decides whether the wash exists.

The Field Is Open. It Will Not Stay Open.

Every condition that preceded the car wash consolidation is now present in truck wash: fragmented supply, one respected labor-based incumbent, settled and formalizing demand, and, as of the last two to three years, automation technology that now handles real-world truck geometry at quality and at speed across a broad range of applications. The one condition still missing is institutional capital, and that absence is the opportunity, not the objection: the equipment reality that justified staying manual has shifted, and the money that just finished professionalizing car wash is actively hunting its next fragmented, real-asset service category.

The last wash consolidation made its biggest winners out of the operators who were already standing on built ground when capital arrived. They were not the competition. They were the product. The next one, whenever it comes, will do the same, and the ground it will pay for is being selected, entitled, and built right now, by whoever decides the window is worth more than the wait.

Building on this thesis?

Big Rig Development Group develops commercial truck and large-vehicle wash facilities nationally, from site identification through certificate of occupancy. If you are evaluating a corridor, a parcel, or an equipment quote, the conversation starts the same way.

Start a ConversationFrequently Asked Questions

Is a truck wash a good investment in 2026?

The category shows the same profile express car wash showed before its consolidation: fragmented supply, settled demand from nearly 15 million registered commercial trucks, and newly viable automation. But returns are decided at the site level, so the honest answer is that a well-sited, well-developed truck wash can be, and a badly sited one cannot. Qualify the site before committing capital.

Is the car wash market saturated?

In the strongest markets, yes. The International Carwash Association's own surveys rank saturation as the industry's top concern, several cities have passed moratoriums on new express tunnels, and platform pricing has compressed from peak multiples. That saturation is pushing operators and investors toward adjacent wash categories, including commercial truck wash.

How is a commercial truck wash different from a car wash?

Same underwriting fundamentals, higher thresholds. A truck wash needs 1 to 3+ usable acres, 40-to-55-foot turning paths for a 53-foot trailer, 180 to 420 feet of stacking, full-movement access on a freight corridor, enhanced wastewater pre-treatment, and a revenue model built on fleet contracts and per-wash volume rather than consumer memberships.

What does it cost to build a truck wash?

Total cost depends almost entirely on land basis, utilities, wastewater requirements, sitework, and equipment configuration. Two projects with identical equipment can differ dramatically in total cost, because development, not equipment, is the largest variable. Credible numbers come from modeling a specific site, not from category averages.

Can automated equipment wash a semi truck or 18-wheeler?

Yes, and this is the recent change that opens the category. Current systems use 3D vehicle profiling to scan each truck's actual contours, handling the mirrors, stacks, and trailer variety that defeated earlier automated equipment. Touchless and hybrid configurations address the brush-damage concern that kept many fleets on hand washing.

What equipment do automated truck washes use?

Touchless high-pressure, friction, and hybrid systems from manufacturers including D&S Car Wash Supply, InterClean, Westmatic, LazrTek, Hydro-Chem Systems, and KKE, supported by 3D vehicle profiling, undercarriage wash, water reclamation, and fleet account software. Configuration should follow the site's vehicle mix and water conditions, not the other way around.

What does a truck wash site require?

Usable acreage, truck-scale turning geometry, deep stacking, full-movement access, freight corridor traffic, adequate water and wastewater capacity, and a zoning posture that accepts heavy vehicle operations. Most parcels fail this screen, which is why site selection comes before equipment selection. A site that fails on geometry fails permanently.

Should a truck stop or travel center add a truck wash?

The land case is proven; the operating case is site-specific. Travel centers sit on validated freight corridor real estate with trucks already on the lot, and equipment manufacturers are now marketing large-vehicle wash systems directly to the travel center industry. Washing remains a water-intensive, environmentally regulated operation outside a travel center's core model, which is why the projects that work pair the operator's site with wash-specific development and engineering discipline.

How long does it take to build a truck wash?

Roughly 18 months from engagement through certificate of occupancy is typical for a well-run project, though timelines are site- and jurisdiction-specific. The sequence: site selection and land control, then entitlement and permitting, then construction and equipment installation. Twelve disciplined months can put an operator under construction on a corridor position that did not exist a year earlier.

Who develops commercial truck wash facilities?

Commercial truck wash facilities are developed by specialized commercial real estate firms or by in-house real estate teams at national brands. Because equipment manufacturers do not handle land acquisition, entitlement, or construction, independent operators typically engage a development partner to carry the project from site to certificate of occupancy. Big Rig Development Group is one such firm, exclusively dedicated to truck and large-vehicle wash facility development, nationally.

Sources and Notes

- Equipment technology and performance figures: manufacturer-published materials and industry equipment guides, including D&S Car Wash Supply (IQ MAX system specifications, cycle time, cost comparison, and NATSO Connect exhibition), InterClean Equipment, Westmatic Corporation (touchless and hybrid systems, water recycling up to 85 percent), Hydro-Chem Systems, LazrTek, and KKE Wash Systems. Throughput ranges (gantry roughly 4 to 6 trucks per hour; drive-through roughly 15 to 20+ per hour) as published in industry equipment guides. All figures are manufacturer- or industry-reported; Big Rig Development Group makes no independent equipment performance claims and is equipment-agnostic.

- Car wash consolidation, valuations, and M&A data: The Deal, Mergermarket / ION Analytics, PE Hub, Raymond James Car Wash Insight, and Car Wash Advisory sector reporting, 2021 to 2026, including H1 2024 transaction count down approximately 46 percent year over year.

- ZIPS Car Wash Chapter 11: public filings and sector press coverage, February 2025 ($654 million in debt, approximately 260 locations).

- Industry sentiment and saturation: International Carwash Association, CAR WASH Pulse, Q4 2025 and Q1 2026 editions; municipal moratorium coverage from Detroit, Cleveland, and Rio Grande Valley news outlets, 2024 to 2026.

- Market structure and format share: Car Wash Advisory, Mordor Intelligence, and sector advisory commentary on express tunnel share and full-service decline.

- Travel center transactions: Berkshire Hathaway's staged acquisition of Pilot Travel Centers (2017 to 2024) and BP's acquisition of TravelCenters of America (2023, approximately $1.3 billion), per company announcements and FreightWaves coverage.

- Fleet washing services transactions: PitchBook and PrivSource records on Fleetwash (ACON Investments) and Kept Companies (DFW Capital Partners).

- Freight data: American Trucking Associations, U.S. Freight Transportation Forecast to 2035; ATA American Trucking Trends 2025; ATA For-Hire Truck Tonnage Index releases through April 2026.

- Fleet wash rationale: trade and fleet maintenance press on corrosion prevention, CSA/DOT inspection outcomes, and fleet appearance and hygiene standards.

- A note on market sizing: published market-size estimates for the truck wash sector vary by several orders of magnitude and contradict one another; this paper intentionally cites none of them. A note on economics: no generic pro forma is published here because truck wash unit economics are site-specific; readers should model actual projects, not category averages.

© 2026 Big Rig Development Group. This paper is provided for general informational purposes and does not constitute investment, legal, or financial advice.